Personal financial planning is essential to achieving financial stability and long-term financial objectives. On the other hand, creating a financial plan may be a complicated process for many people. This is because it requires a thorough understanding of many financial concepts, such as investing, debt management, insurance, retirement, tax, and estate planning. Additionally, the financial business is continually changing, making it challenging to keep up with the latest advances.

We will go deeper into the definition and purpose of a financial plan. Also, look at some of the most important aspects of a financial plan, such as risk management, estate planning, tax planning, and retirement planning. Discuss the benefits of having a financial plan and when to make one. Also go through how to establish a financial plan, including working with licensed financial consultants or financial planners near me.

What is Financial Plan?

A financial plan is a detailed strategy for reaching long-term financial objectives. It entails examining a person’s financial status, identifying financial objectives, and creating a plan for achieving those goals. Investment strategies, retirement planning, debt management, tax planning, estate planning, and risk management are all examples of financial plans.

Selecting particular financial goals is a critical component of a financial strategy. These goals can be short-term, such as saving for an emergency fund or a down payment on a house, or long-term, such as saving for retirement or paying for a child’s school. After determining these goals, a financial plan explains the procedures necessary to accomplish them.

Creating a budget is also part of developing a financial strategy. A budget is a precise plan for a given period’s revenue and spending. It entails assessing existing spending patterns and identifying places where expenditures might be cut or eliminated. A budget is essential to a financial plan because it offers a structure for managing costs and meeting financial objectives.

Formulating an investing strategy is another critical component of a financial plan. This method is customized to a person’s investing goals, risk tolerance, and time horizon. It includes picking personal finance investing like equities, bonds, mutual funds, and exchange-traded funds (ETFs). The investing technique aims to maximize profits while reducing risk.

Purpose of a Financial Plan

A financial plan aims to equip individuals with a road map for reaching their long-term financial goals. It includes all areas of personal finance, such as investing, debt management, retirement planning, and insurance. A financial plan’s primary goal is to assist individuals in making educated financial decisions that will lead to financial stability and prosperity.

One of the critical advantages of having a financial plan is that it reduces financial stress. A well-crafted personal financial plan may give individuals peace of mind by ensuring they have a clear plan to achieve their financial objectives. It can assist people in prioritizing their spending, reducing financial waste, and identifying future financial problems.

A financial strategy should also identify potential risks and suggest solutions to reduce them. Risk management techniques, such as insurance coverage, emergency savings, and debt reduction strategies, are all part of a comprehensive financial strategy. This can assist people in avoiding financial disaster in the case of an unexpected expenditure or loss of income.

Understanding Financial Plans and their Key Components

Knowing the essential components of a financial plan is critical for building a complete and effective financial strategy. A financial plan is often comprised of numerous interconnected parts, each with its own goals and techniques.

-

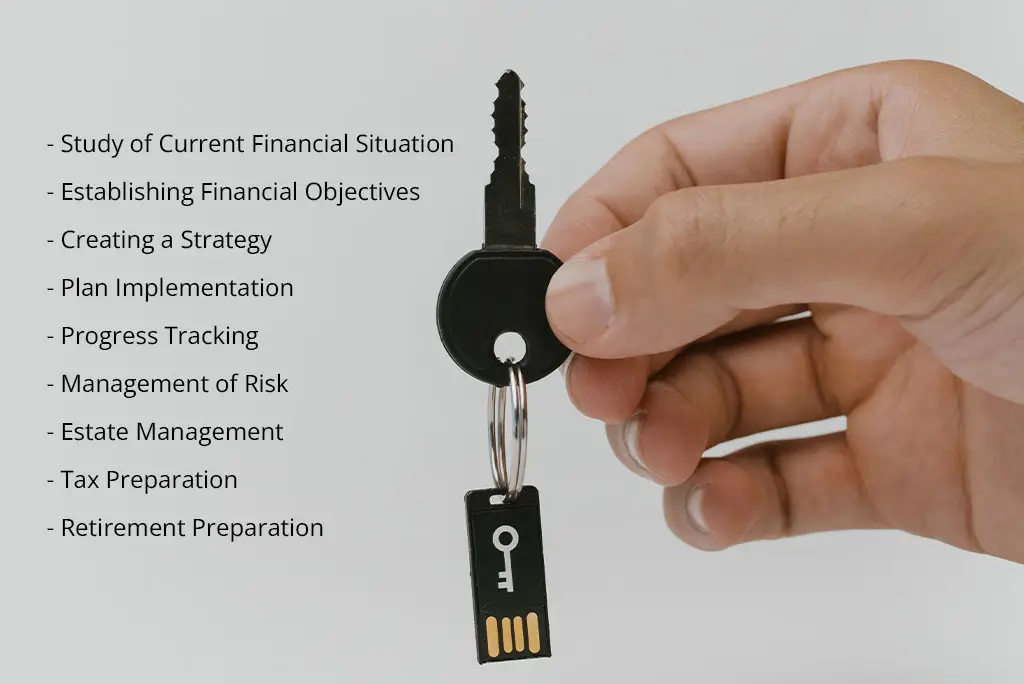

Study of Current Financial Situation

The first stage in developing a financial plan is determining one’s present financial situation. Income, spending, assets, obligations, and cash flow are all examined in this study. This data serves as the foundation for creating a complete financial strategy.

-

Establishing Financial Objectives

The following stage is to establish and create achievable financial objectives. These objectives might include purchasing a home, saving for retirement, paying off debt, or establishing an emergency fund. Setting clear, measurable, attainable, relevant, and time-bound goals is essential.

-

Creating a Strategy

The strategy specifies the procedures required to reach each financial target. For example, a method for purchasing a home may include the following:

- Setting aside a particular amount of money each month.

- Boosting one’s credit score.

- Researching mortgage choices.

Income, spending, savings, investments, and risk management should all be included in a holistic strategy.

-

Plan Implementation

Once a strategy has been established, the plan must be implemented. This entails making substantial efforts toward each financial objective. For example, if the aim is to pay off debt, a strategy may include creating a debt repayment plan and cutting back on expenditures.

-

Progress Tracking

Monitoring the financial plan’s progress is critical to ensuring that it stays on track. Frequent financial plan reviews enable people to make required modifications and guarantee that the strategy remains relevant and successful.

-

Management of Risk

Risk management is an essential component of every financial strategy. It entails recognizing possible dangers and devising threats methods. This involves debt management, sufficient insurance coverage, and financial diversity.

-

Estate Management

Estate planning is the process of arranging assets for transfer after death. A will, power of attorney, and healthcare directive are all part of a comprehensive estate plan. It guarantees that one’s assets are transferred by one’s intentions and lessens the financial strain on surviving loved ones.

-

Tax Preparation

Tax planning entails developing techniques to reduce tax bills while increasing after-tax revenue. This involves using tax-advantaged investment accounts, deductions, and credits.

-

Retirement Preparation

Retirement planning is creating a plan to ensure a pleasant retirement. It includes establishing retirement objectives, predicting retirement costs, and devising a savings strategy. A thorough retirement plan considers retirement income sources, including social security and pensions.

Benefits of a Financial Plan

A personal financial plan is a strategy to accomplish long-term financial objectives that gives various advantages to those who follow it. Here are some of the essential advantages of a well-crafted financial plan

-

Offers a clear roadmap to reaching financial objectives

A personal financial plan assists individuals in identifying their financial objectives, prioritizing costs, and developing a savings strategy to help them reach those goals. It assists customers in tracking their progress and staying on track by offering a clear route to reaching their financial goals.

-

Financial stress is reduced

Financial stress is a significant source of worry and may considerably influence a person’s well-being. A financial plan alleviates financial stress by giving an organized approach to money management, minimizing ambiguity and anxiety.

-

Identifies possible risks

A financial plan evaluates a person’s present financial condition, identifies prospective dangers, and suggests ways to manage those risks. This enables individuals to plan for and mitigate the impact of unforeseen costs, such as medical bills or job loss, on their financial stability.

-

Enhances investment returns

A financial plan contains an investing strategy that is matched to a person’s risk tolerance and financial objectives. This enables individuals to make more educated financial decisions, improving long-term investment returns.

-

Enables making well-informed decisions

A personal financial plan gives people a thorough assessment of their financial condition and a clear grasp of their financial aspirations. This helps consumers make educated financial decisions, such as buying a property, taking out a loan, or investing in a specific asset class.

-

Allows for the effective utilization of resources

A personal financial plan assists individuals in prioritizing their spending and using their financial resources most. This guarantees they are spending their money correctly and not overspending in areas that may not align with their long-term financial objectives.

When to Create a Financial Plan

A financial plan is a dynamic process that must be modified frequently to reflect financial objectives, priorities, and circumstances changes. While there is no set schedule for developing a financial plan, certain life events or situations should prompt a review or update of an existing plan or the development of a new plan entirely.

1. Marriage

Marriage is a momentous event that changes personal and financial aspirations and priorities. Developing a financial plan together may assist couples in aligning their financial objectives, prioritizing spending, and creating a plan to accomplish those goals.

2. Having a family

A new baby brings pleasure and excitement but also increases costs and obligations. Developing a financial plan that accounts for additional expenditures such as daycare, schooling, and insurance may assist parents in planning for the future and ensuring that they are on pace to meet their long-term financial objectives.

3. Change of career

A career shift, whether deliberate or involuntary, can have a substantial financial impact. Individuals can use a financial plan to examine the financial implications of a professional change, such as income, benefits, and retirement savings, and establish a strategy to modify their finances accordingly.

4. Purchasing a Home

Home purchasing is a substantial financial investment that necessitates careful planning and budgeting. A financial plan may assist people in determining how much they can afford to spend on a property, assessing the impact of a mortgage on their finances, and developing a strategy to pay off their mortgage as soon as feasible.

5. Retirement

One of the most critical areas of personal finance is retirement planning. A financial plan can assist individuals in assessing their retirement goals, estimating their retirement needs, and developing a retirement savings strategy.

6. Receiving or inheriting a considerable quantity of money

Getting a lot of money, such as an inheritance or settlement, can be stressful. Having a financial plan to manage money and guarantee that it is utilized sensibly is critical.

7. A financial disaster is coming

If you are in the midst of a financial crisis, such as a job loss or unanticipated medical bills, it is critical to developing a financial plan to assist you in getting back on track. This might entail budgeting, prioritizing spending, and looking for ways to lower your debt.

Conclusion

Having a financial plan is essential to long-term financial success. Knowing its essential components, and how to build one is necessary for financial stability. Working with a certified financial advisor near me can give you the experience and assistance you need to establish a successful financial plan.